Two 100K accounts, opposite payout profiles

Two prop accounts, both 100K, both built from systematic strategies. One pays out more than twice as often as the other. Most traders would pick the frequent one without reading the second line. The second line is the whole story.

Data window: backtest + live sample (Jun 2025 – May 2026) · Monte Carlo: 1,500 paths × 3-year horizon · Last verified: June 2026 · Figures refresh quarterly.

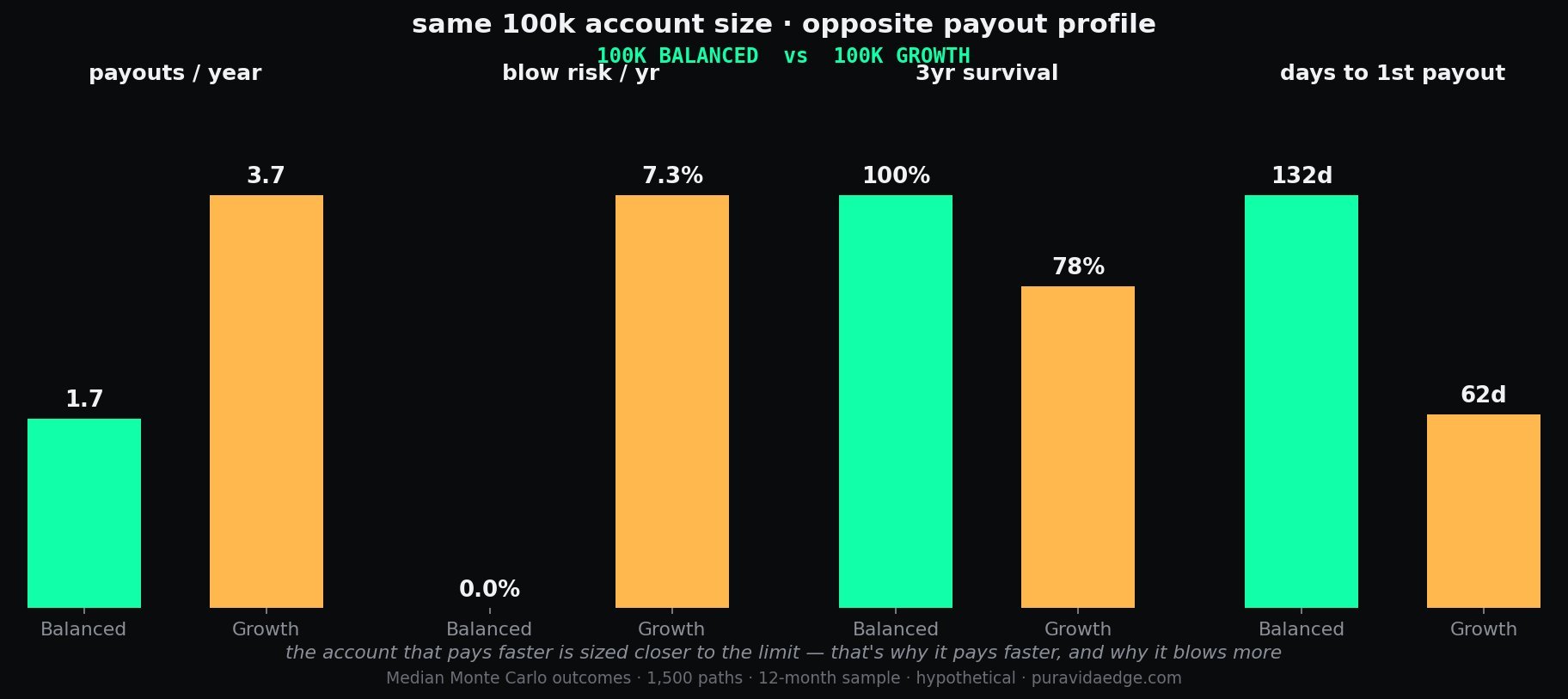

Both accounts are 100K. Both run systematic strategies with hard-coded entries, targets and exits. On paper they belong in the same bucket. The payout column splits them in half: the Balanced 100K pays out about 1.7 times a year, the Growth 100K about 3.7.

Net is the one number the chart leaves out, and it runs the other way: the Balanced 100K models about $11k a year, the Growth 100K about $23k. That is the pull toward Growth. The other four bars are the bill.

What the frequent one trades away

Faster and larger reads as strictly better until you price the failures. Roughly one in five Growth runs does not survive the three-year horizon; the Balanced version loses closer to one in a thousand. That is the trade. Payout frequency is a function of how hard the account pushes the drawdown buffer, and pushing the buffer is the same lever that lifts the blow rate. You do not get to move one without moving the other.

Why frequency is the wrong headline

A payout you never reach because the account blew in month two is worth nothing. So the honest comparison is not payouts per year, it is payouts per year weighted by the odds of still being funded to collect them. On that math the gap between these two narrows hard, and for an expensive two-phase evaluation it can flip the ranking entirely.

Which one is yours

Match the profile to the cost of failure, not the size of the payout. Cheap eval, fast reset, capital you can redeploy without flinching: the Growth cadence is rational, close to a throughput bet across resets. Expensive eval, or capital and confidence that a blow would dent: the Balanced account's slower, near-unkillable cycle is exactly what you are paying for. Most traders should start Balanced and earn the right to push. The full risk side sits in the blow rate data, and the profile framing in Balanced vs Growth.

FAQ

Does paying out more often mean making more money?

Not by itself. The more frequent account here also carries a far higher blow rate, so expected cash depends on how often you survive long enough to collect. Frequency and survival pull in opposite directions.

Which 100K portfolio should I pick?

Start Balanced if a blown account would set you back financially or psychologically. Choose Growth only when resets are cheap and you have evidence of your own tolerance across a few cycles.

Not financial advice. Performance figures are hypothetical, modeled Monte Carlo outputs (P50 medians; backtest + live sample, ~1,500 paths). Past performance does not guarantee future results. Verify every prop-firm rule with the firm directly. Puravida Edge is a product of Pura Vida Connections LLC.