Why prop firm portfolios should be sized off the drawdown limit, not the return target

Most traders pick a size that hits the profit target fast and treat the drawdown limit as a thing to avoid. That is backwards. Sizing off the limit first, so a normal bad stretch never gets close to the floor, is what actually keeps a funded account alive. Here is the mechanic, and the Monte Carlo data behind it.

⚠ Rules change often. Prop-firm drawdown models and Terms of Service change frequently. Always verify your specific account's rules before deploying any strategy. Figures here were checked June 2026.

Sizing is where most funded accounts are won or lost, and the framing almost everyone uses is upside-down. The drawdown limit is not an obstacle to dodge on the way to the target. It is the number the whole position size should be built around.

The two floors behave differently

Before sizing, the drawdown model matters. On end-of-day trailing, the floor only moves off the closing balance. Intraday swings do not touch it. A position can take heat during the session and the floor stays put, as long as the account closes acceptably.

On intraday trailing it works the opposite way. The floor chases the highest unrealized point of the day, so a pullback on a trade that was green can breach the account even if it later recovers. Completely different risk, and it demands completely different sizing. Everything below assumes EOD trailing, the futures-industry standard. The full EOD vs intraday comparison covers why.

Size off the limit, not the target

Here is the part most people get backwards. They size for the return: pick a size that reaches the profit target quickly, then hope the drawdown stays out of the way. The better approach goes the other direction. Size off the limit first, so a normal losing stretch never approaches the floor, then let the return be whatever it ends up being above that.

The reason this works on EOD specifically is that the floor is forgiving intraday. The position can move against you during the session as long as it closes okay. So the number that matters is the close-to-close drawdown, not the worst tick. Size for that, and a routine bad run leaves room instead of ending the account.

But it only holds if the strategy genuinely respects the limit across many possible sequences, not just the one backtest that happened to play out. A single clean history proves nothing about the next bad stretch. That is where validation comes in.

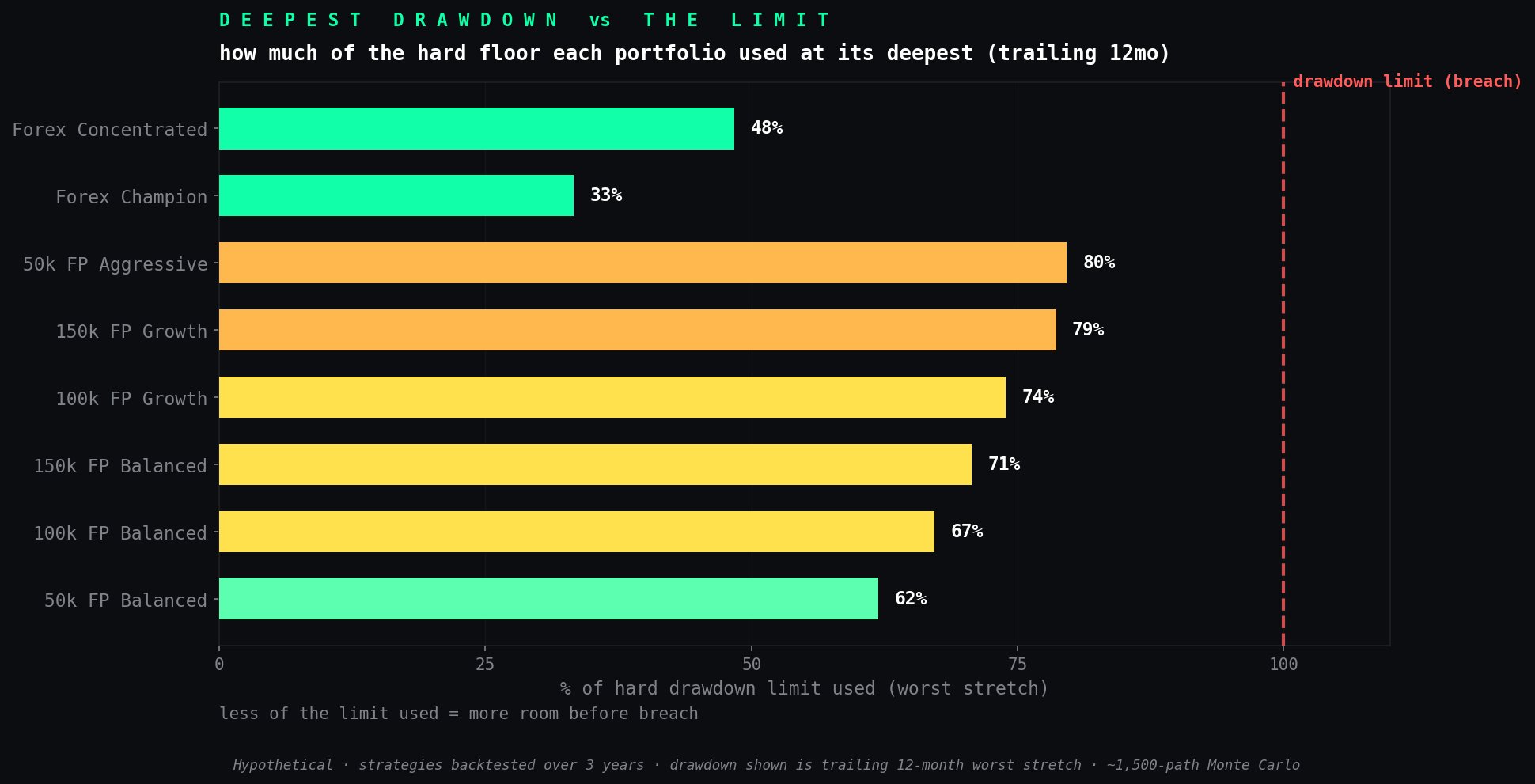

What the Monte Carlo data shows

Every Puravida Edge portfolio is built around this. Each is backtested over three years, then run through roughly 1,500 Monte Carlo paths on top. The number that gets watched is not the return. It is how much of the hard drawdown limit each portfolio ate in its worst stretches.

The chart above is the trailing 12-month window. The balanced futures portfolios top out around 60 to 70 percent of the limit used at their deepest. They do not sit right on the floor. There is room left even on a bad run, and that is the design, not luck. The more aggressive growth portfolios run hotter, into the high 70s and low 80s, which is the deliberate trade for faster payouts and higher blow rates.

The forex swing side uses even less, with the deepest drawdown around a third of the limit on the Champion configuration. Most of that comes from the strategies not correlating, so they do not all bleed at the same time. Learn how to size against the floor step by step, or see the instruments that fit EOD trailing best.

The limit is the thing you size from

So the drawdown limit ends up being the thing the size is built from, not the thing to dodge. Size so the worst expected stretch leaves room below the floor, and the breach math mostly takes care of itself. The return follows from a survivable size rather than dictating a reckless one.

One more piece makes the close-to-close number reliable. Puravida Edge futures presets flatten before the session close via an end-of-day guard, so settlement is clean and no overnight gap moves the mark. That keeps the drawdown predictable, which is exactly the figure being sized against. For the mechanics of how that floor moves, the trailing vs static vs daily-loss breakdown is a useful next read.

FAQ

Should I size for the profit target or the drawdown limit?

Size off the drawdown limit first. Pick a size where a normal losing stretch never approaches the floor, then let the return be whatever it is above that. Sizing for the target and treating the limit as a thing to avoid is backwards, because one normal bad run can breach you before the target is ever reached.

How much of the drawdown limit is safe to use?

The deepest drawdown should leave clear room below the hard limit. In the trailing 12-month window the balanced futures portfolios topped out around 60 to 70 percent of the limit, and the forex swing portfolios used about a third to a half. Room left on a bad run is the design, not luck.

Why does sizing off the limit work better on EOD trailing?

On end-of-day trailing the floor only moves off your closing balance, so intraday heat does not breach you as long as the position closes acceptably. That lets you size for the close-to-close drawdown rather than the worst tick, which is more forgiving than intraday trailing where the floor chases your highest unrealized point.

Does flattening before the close matter for sizing?

Yes. Flattening before the session close means settlement is clean with no overnight gap moving the mark against you. It keeps the close-to-close drawdown predictable, which is exactly the number you are sizing against on EOD trailing.

Not financial advice. Performance figures are hypothetical, modeled outputs (3-year backtest with ~1,500-path Monte Carlo; drawdown shown is the trailing 12-month worst stretch). Past performance does not guarantee future results. Prop-firm Terms of Service compliance is your responsibility — verify every rule with the firm directly.