Open

Range Break

Range expansion at open + retest + directional breakouts. Four-instrument coverage (MNQ, MGC, NAS, XAU) with 5-minute timeframe execution and EOD guard. Backtest Q2'25–Q1'26 + live Q2'26: best PF 5.25 (NAS), combined +$53,392 backtest / +$17,014 live at 100K presets.

At a glance

Best-performing instrument per metric (max 3 from one instrument). Rolling last 12 months at 100K preset; forecast metrics from 1,500-path Monte Carlo, 3-year horizon. Viability 3y = % of MC paths that never hit the hard drawdown. Payouts : blow = payouts per one account blow over 3y. TTP = median days to first payout.

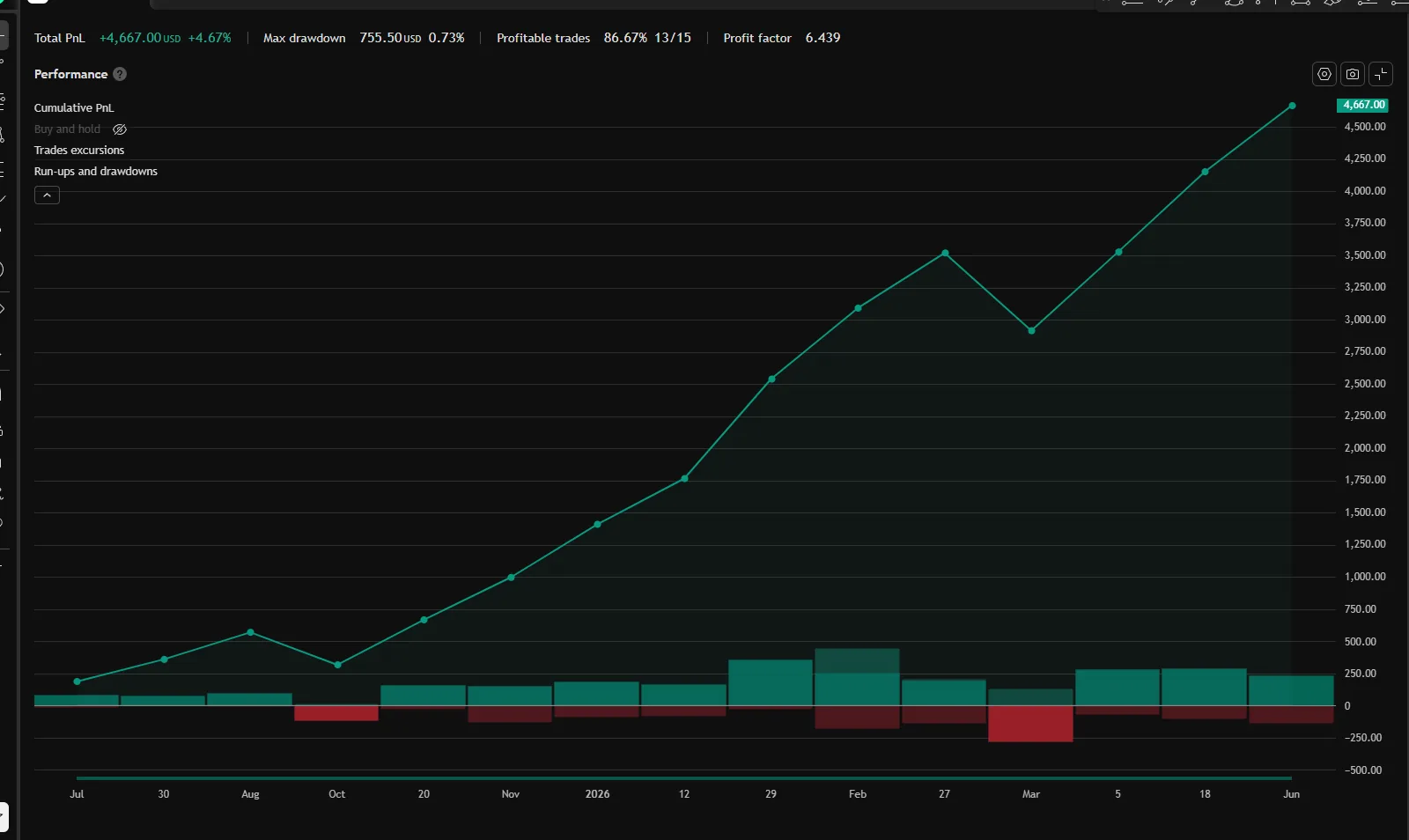

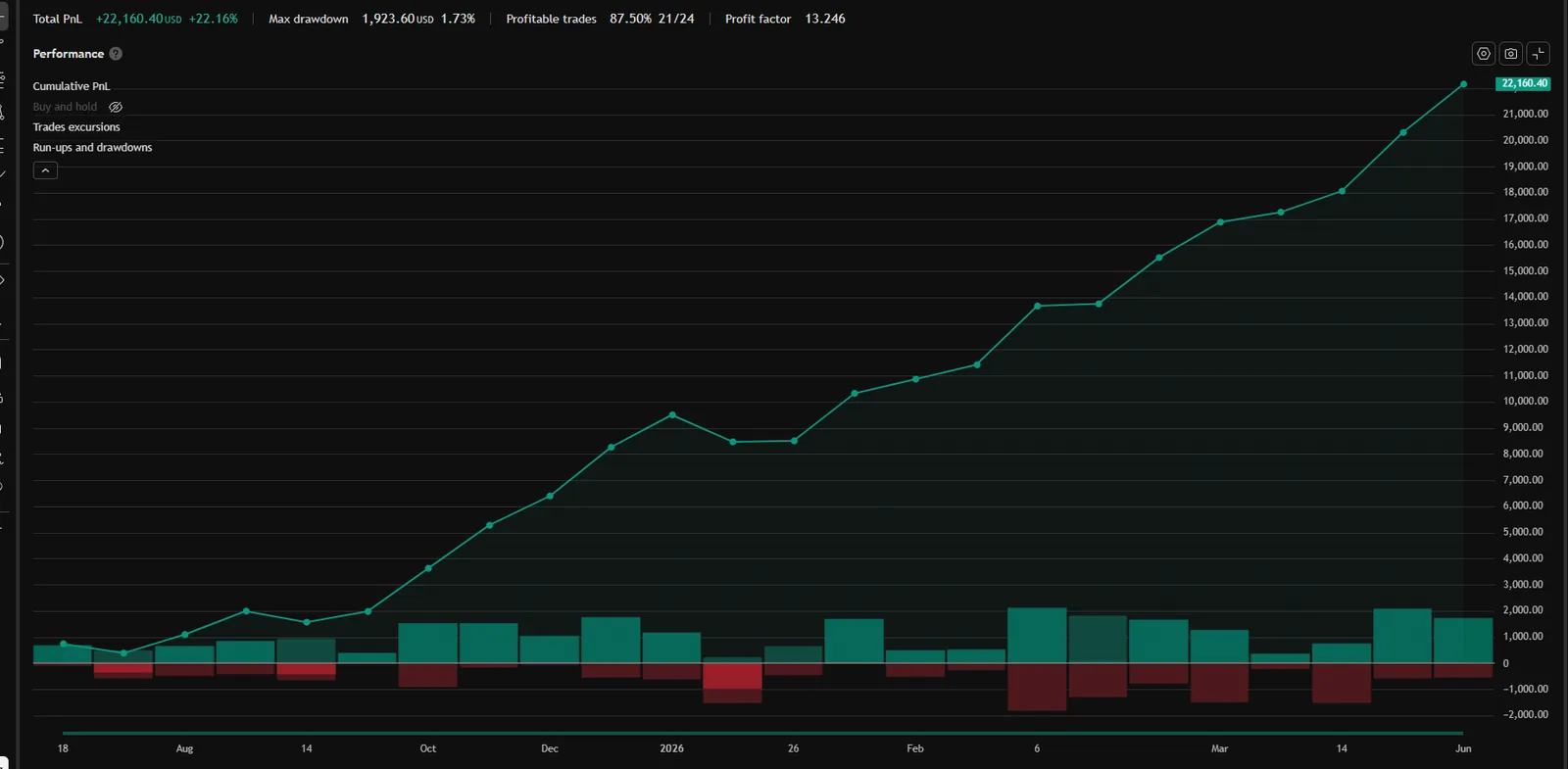

Equity curve · backtest + live

Daily P&L applied to the $100,000 starting balance at the 100K preset (2 ct), log scale. Gray = pre-publication (2025-04-01 → 2026-03-31); accent = live (2026-04-01 → 2026-06-30).

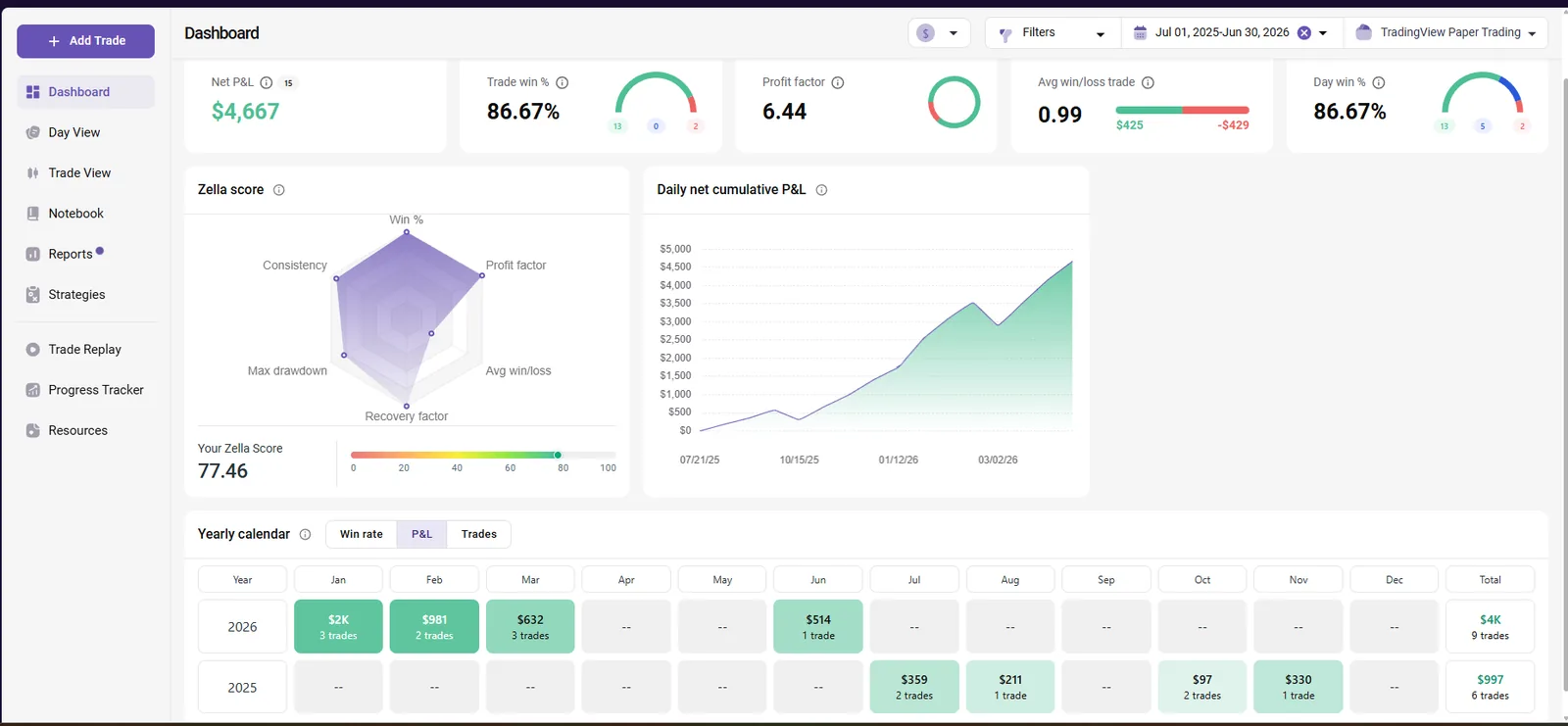

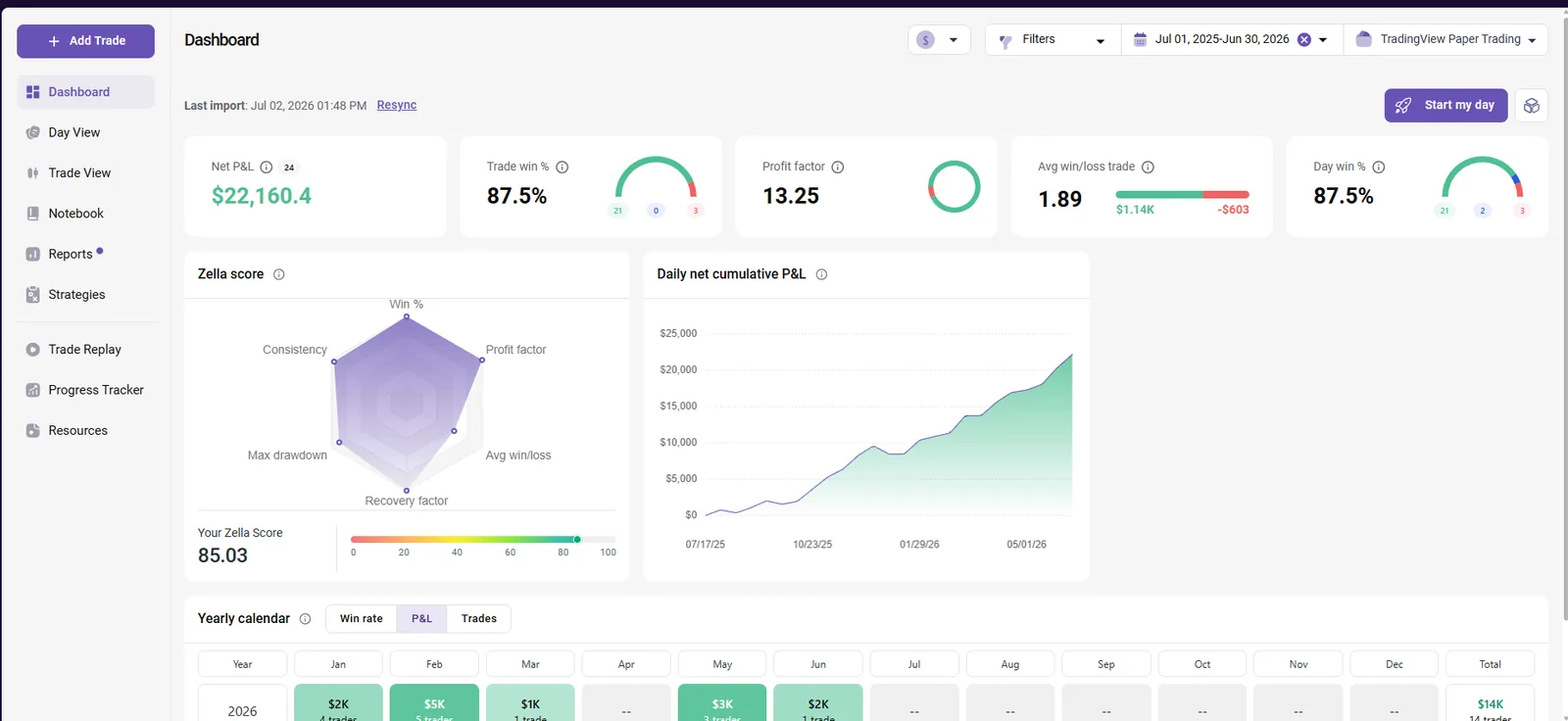

TradingView performance summary · last 4 quarters (Q3'25 — Q2'26)

Quarterly breakdown

| Quarter | Net | WR | Trades | Max DD (EOD) |

|---|---|---|---|---|

| Q3'25 | +$1,514 | 100.0% | 5 | $0 |

| Q4'25 | +$854 | 66.7% | 3 | $506 |

| Q1'26 | +$6,312 | 87.5% | 8 | $1,210 |

| Q2'26 live | +$1,028 | 100.0% | 1 | $0 |

Drawdowns are EOD basis; intrabar peak-to-trough runs higher.

Stats · backtest

| Avg win / loss | W:L ratio | Largest win / loss | Max DD EOD | Sharpe | Sortino | Calmar | Avg bars |

|---|---|---|---|---|---|---|---|

| $1,027 / $-788 | 1.30 | $1,700 / $-1,475 | $2,768 (2.8%) | 3.18 (4.44 live) | 1.83 | 6.23 | 35.0 |

Account sizing · Monte Carlo 1,500 paths × 3y

| Account | Qty | Blow/y | Viability | Pass:Blow | TTP | Pay/y | Net/y P10 | P50 | P90 | P50 after split |

|---|---|---|---|---|---|---|---|---|---|---|

| 50K | 3 ct | 0.3% | 99.2% | 2976:1 | 71d | 8.0 | $7,303 | $9,345 | $11,524 | $8,410 |

| 100K | 5 ct | 0.4% | 98.8% | 2141:1 | 59d | 8.7 | $12,133 | $15,570 | $19,207 | $14,013 |

| 150K | 8 ct | 0.4% | 98.7% | 2105:1 | 52d | 9.0 | $19,382 | $24,913 | $30,730 | $22,422 |

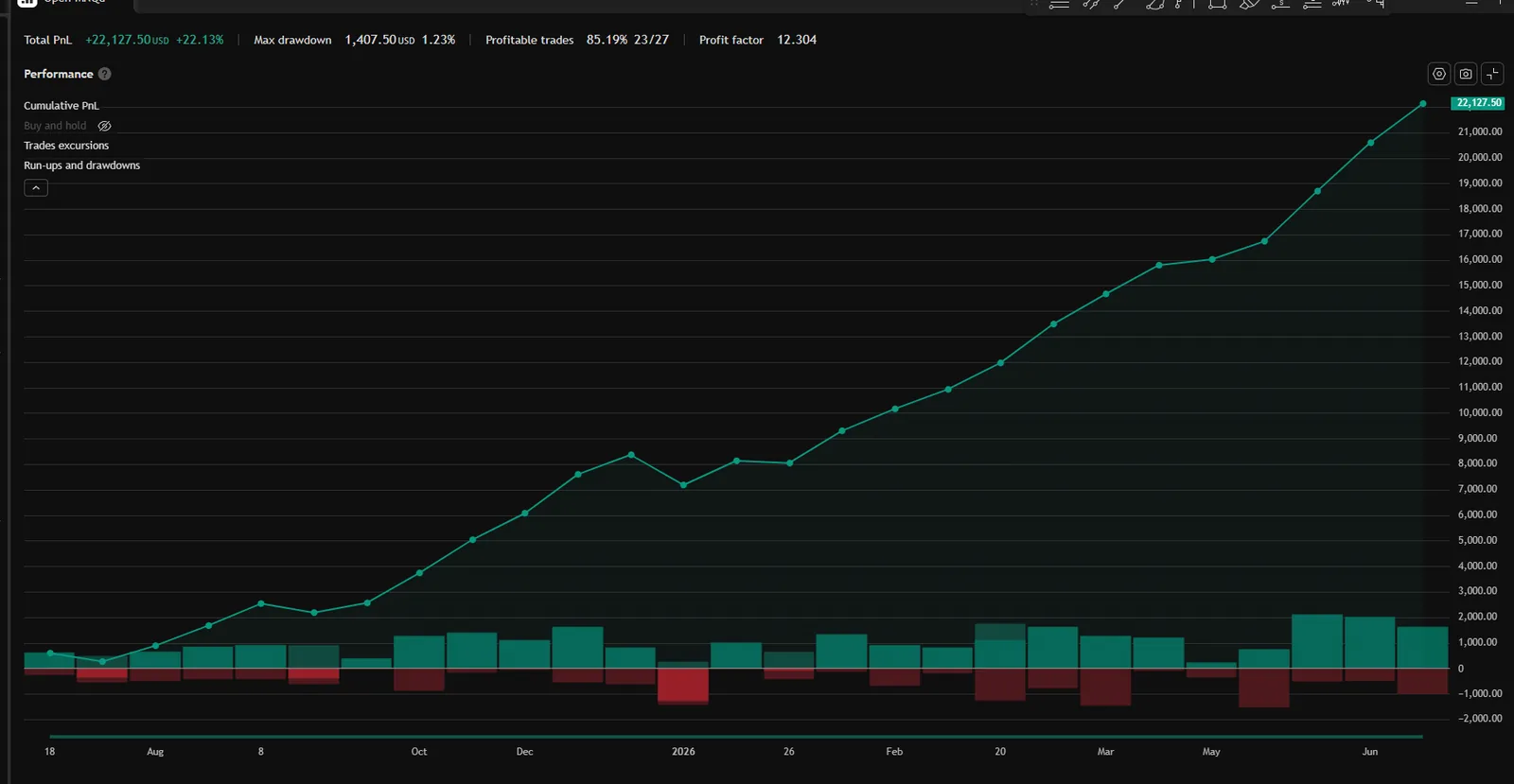

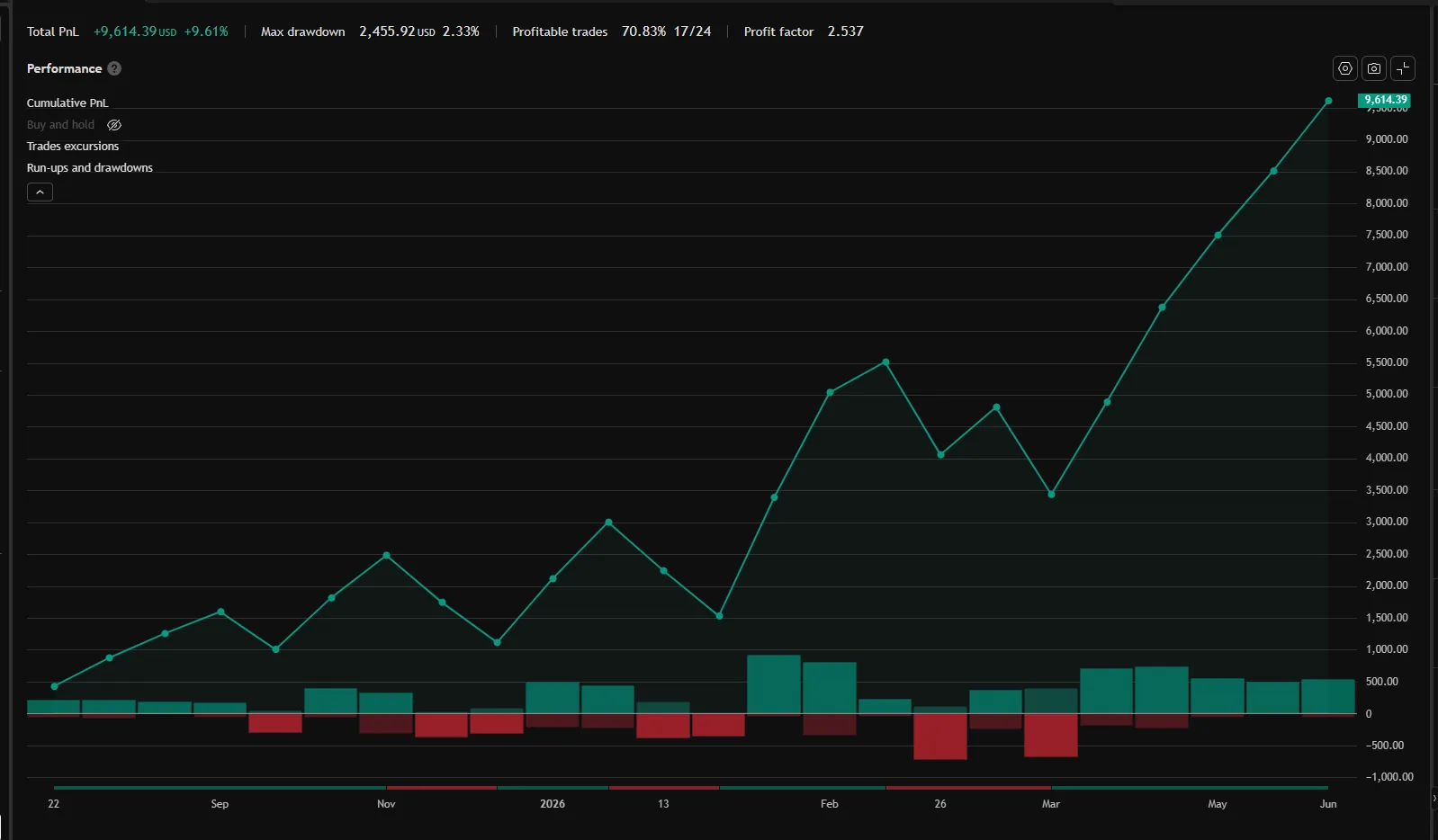

Equity curve · backtest + live

Daily P&L applied to the $100,000 starting balance at the 100K preset (5 ct), log scale. Gray = pre-publication (2025-04-01 → 2026-03-31); accent = live (2026-04-01 → 2026-06-30).

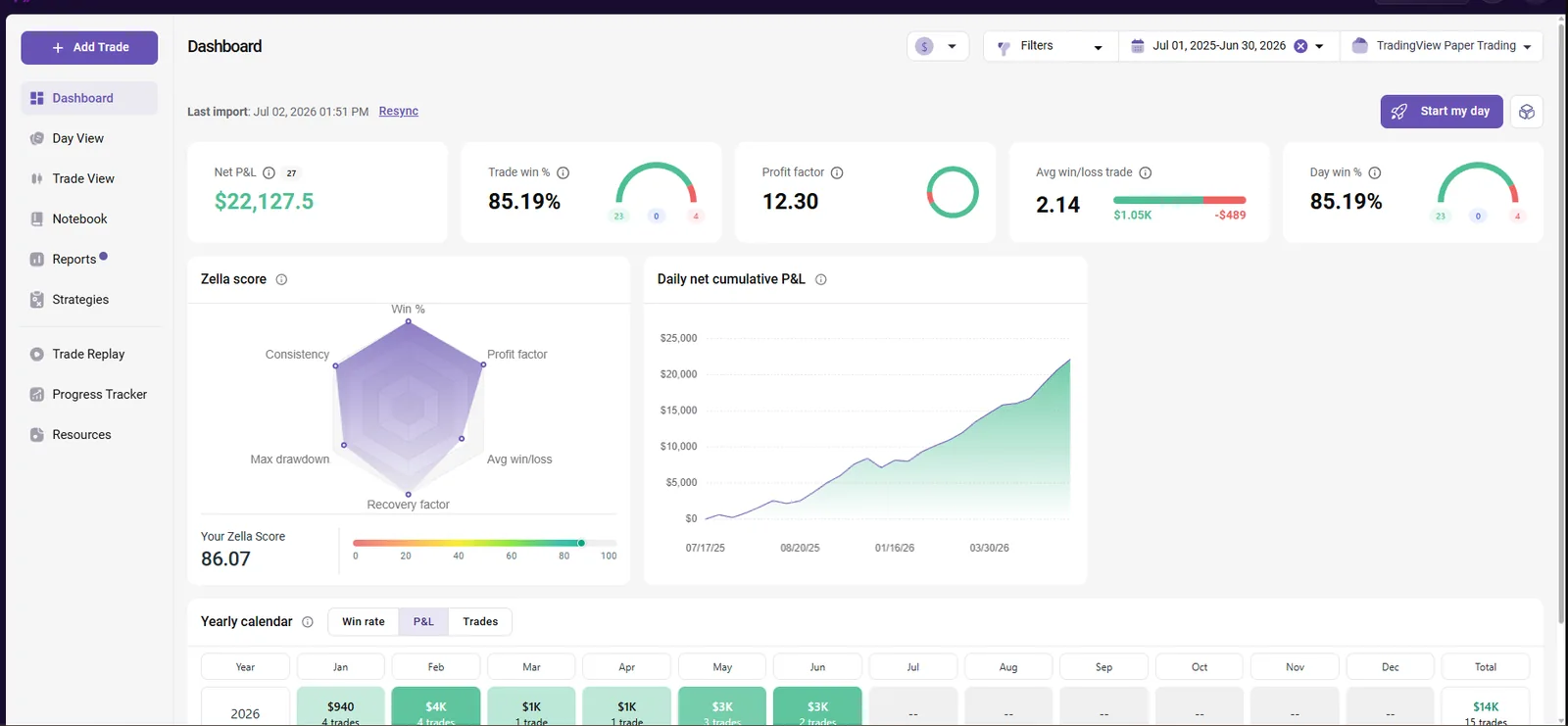

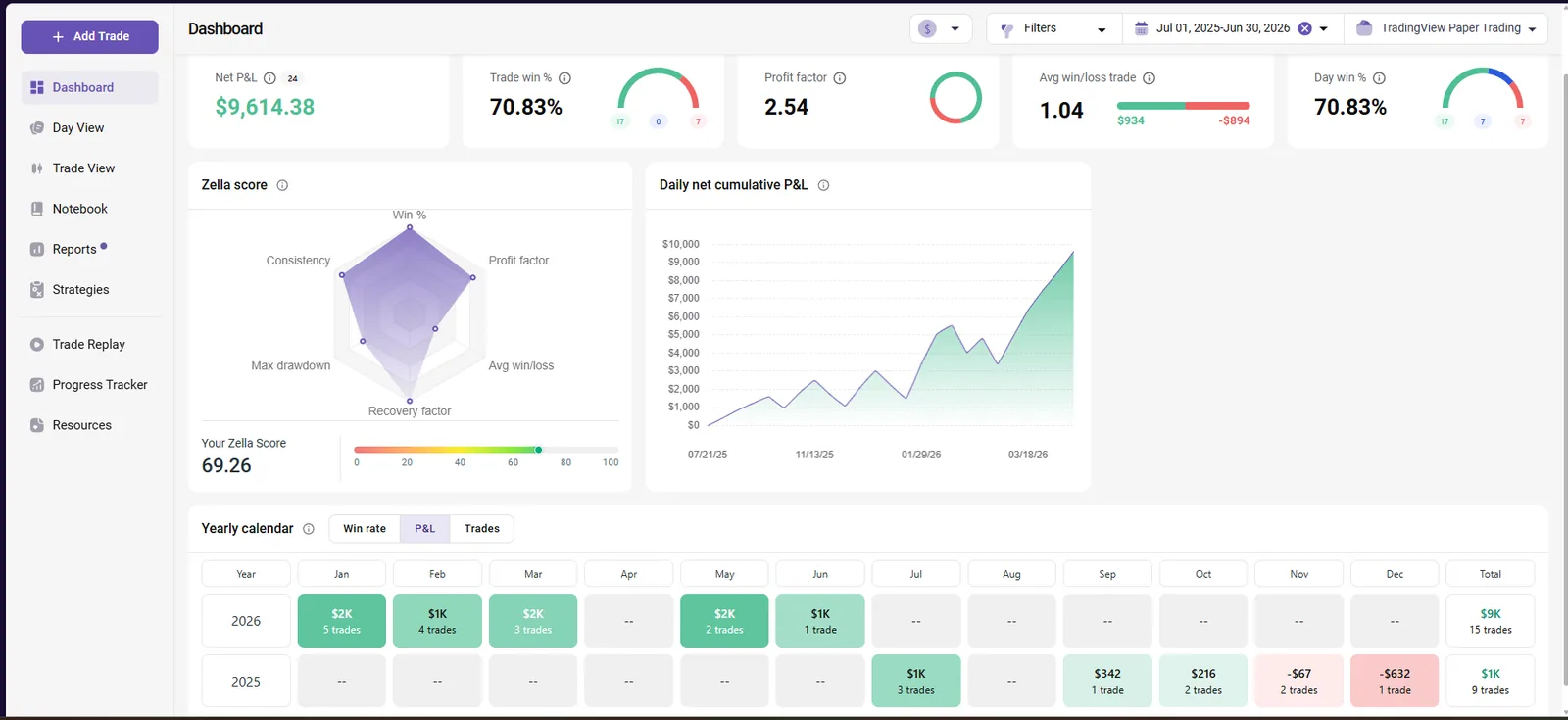

TradingView performance summary · last 4 quarters (Q3'25 — Q2'26)

Quarterly breakdown

| Quarter | Net | WR | Trades | Max DD (EOD) |

|---|---|---|---|---|

| Q3'25 | +$1,265 | 62.5% | 8 | $1,292 |

| Q4'25 | +$5,808 | 100.0% | 5 | $0 |

| Q1'26 | +$6,302 | 77.8% | 9 | $1,185 |

| Q2'26 live | +$7,460 | 100.0% | 6 | $0 |

Drawdowns are EOD basis; intrabar peak-to-trough runs higher.

Stats · backtest

| Avg win / loss | W:L ratio | Largest win / loss | Max DD EOD | Sharpe | Sortino | Calmar | Avg bars |

|---|---|---|---|---|---|---|---|

| $743 / $-672 | 1.11 | $1,548 / $-1,210 | $1,210 (1.2%) | 2.18 (1.97 live) | 1.30 | 6.15 | 74.0 |

Account sizing · Monte Carlo 1,500 paths × 3y

| Account | Qty | Blow/y | Viability | Pass:Blow | TTP | Pay/y | Net/y P10 | P50 | P90 | P50 after split |

|---|---|---|---|---|---|---|---|---|---|---|

| 50K | 1 ct | 0.0% | 100.0% | >9999:1 | 182d | 4.0 | $2,612 | $3,567 | $4,615 | $3,210 |

| 100K | 2 ct | 0.1% | 99.7% | 5984:1 | 130d | 5.3 | $5,216 | $7,130 | $9,230 | $6,417 |

| 150K | 3 ct | 0.1% | 99.7% | 7106:1 | 121d | 6.3 | $7,823 | $10,695 | $13,844 | $9,626 |

Equity curve · backtest + live

Daily P&L applied to the $100,000 starting balance at the 100K preset (12 lot), log scale. Gray = pre-publication (2025-04-01 → 2026-03-31); accent = live (2026-04-01 → 2026-06-30).

TradingView performance summary · last 4 quarters (Q3'25 — Q2'26)

Quarterly breakdown

| Quarter | Net | WR | Trades | Max DD (EOD) |

|---|---|---|---|---|

| Q3'25 | +$439 | 57.1% | 7 | $1,536 |

| Q4'25 | +$6,283 | 100.0% | 4 | $0 |

| Q1'26 | +$8,617 | 90.0% | 10 | $1,031 |

| Q2'26 live | +$5,285 | 100.0% | 4 | $0 |

Drawdowns are EOD basis; intrabar peak-to-trough runs higher.

Stats · backtest

| Avg win / loss | W:L ratio | Largest win / loss | Max DD EOD | Sharpe | Sortino | Calmar | Avg bars |

|---|---|---|---|---|---|---|---|

| $1,204 / $-1,008 | 1.19 | $2,250 / $-1,696 | $3,232 (3.2%) | 3.09 (3.48 live) | 2.11 | 6.41 | 38.0 |

Account sizing · Monte Carlo 1,500 paths × 3y

| Account | Qty | Blow/y | Viability | Pass:Blow | TTP | Pay/y | Net/y P10 | P50 | P90 | P50 after split |

|---|---|---|---|---|---|---|---|---|---|---|

| 50K | 6 lot | 0.0% | 100.0% | >9999:1 | 33d | 6.0 | $6,344 | $8,264 | $10,212 | $7,024 |

| 100K | 12 lot | 0.0% | 100.0% | >9999:1 | 33d | 6.0 | $12,687 | $16,528 | $20,425 | $14,049 |

| 200K | 24 lot | 0.0% | 100.0% | >9999:1 | 33d | 6.0 | $25,375 | $33,057 | $40,849 | $28,098 |

Equity curve · backtest + live

Daily P&L applied to the $100,000 starting balance at the 100K preset (0.25 lot), log scale. Gray = pre-publication (2025-04-01 → 2026-03-31); accent = live (2026-04-01 → 2026-06-30).

TradingView performance summary · last 4 quarters (Q3'25 — Q2'26)

Quarterly breakdown

| Quarter | Net | WR | Trades | Max DD (EOD) |

|---|---|---|---|---|

| Q3'25 | +$2,718 | 100.0% | 7 | $0 |

| Q4'25 | -$484 | 40.0% | 5 | $1,368 |

| Q1'26 | +$5,260 | 66.7% | 12 | $2,078 |

| Q2'26 live | +$3,241 | 100.0% | 3 | $0 |

Drawdowns are EOD basis; intrabar peak-to-trough runs higher.

Stats · backtest

| Avg win / loss | W:L ratio | Largest win / loss | Max DD EOD | Sharpe | Sortino | Calmar | Avg bars |

|---|---|---|---|---|---|---|---|

| $809 / $-820 | 0.99 | $1,861 / $-1,455 | $2,078 (2.1%) | 1.33 (3.46 live) | 1.12 | 2.96 | 51.0 |

Account sizing · Monte Carlo 1,500 paths × 3y

| Account | Qty | Blow/y | Viability | Pass:Blow | TTP | Pay/y | Net/y P10 | P50 | P90 | P50 after split |

|---|---|---|---|---|---|---|---|---|---|---|

| 50K | 0.12 lot | 2.4% | 92.7% | 102:1 | 61d | 2.7 | $1,915 | $3,550 | $5,060 | $3,018 |

| 100K | 0.25 lot | 0.0% | 99.9% | >9999:1 | 60d | 3.0 | $4,496 | $7,462 | $10,545 | $6,343 |

| 200K | 0.5 lot | 0.0% | 99.9% | >9999:1 | 60d | 3.0 | $8,993 | $14,924 | $21,091 | $12,685 |

Risk disclosure

Backtest Q2'25–Q1'26 plus live Q2'26 at the stated presets. Past performance, simulated or live, does not guarantee future results. Futures and CFD trading involves substantial risk of loss; prop-firm accounts add breach rules (daily/EOD drawdown) that can terminate an account regardless of long-term edge. Size accordingly.

How Open works

Open targets the most reliable intraday pattern in futures trading — the range expansion that occurs in the first 90 minutes after market open. After a defined opening range establishes, the strategy waits for a breakout, then a retest of the broken level, then re-entry confirmation. Three legs of confirmation before any position is opened.

The strategy is directional-agnostic and works across four instruments (MNQ, MGC, NAS, XAU). On MNQ it produced 27 trades over 12 months with high conviction (PF 4.46, 77.8% win rate). On MGC it produced 114 trades with moderate per-trade payoff (PF 2.03).

Exits use a hybrid stop-and-target system: fixed initial stop at the failed retest level, profit target calculated from session-derived volatility (ATR-based), plus an EOD GUARD that closes any open position 5 minutes before close to avoid overnight exposure. Holding periods average ~60 bars on 5m timeframe — roughly 5 hours.

Sizing is calibrated for EOD Trailing prop firm accounts, where the trailing drawdown locks at close-of-day. Growth variants (100K+ MGC, 150K MNQ) carry elevated blow rates (14–20%/y) reflecting the trade-off: bigger size, faster funding, higher tail risk. Conservative variants (50K accounts) stay below 11%/y blow rate.

How these numbers were calculated

Trade counts, win rates, profit factors, drawdown values come directly from TradingView Strategy Tester for the baseline preset shown. Verify by running the strategy in your own TradingView after purchase — numbers match 1:1.

DD%, SL%, Pass:Blow ratio and percentile breakdowns are computed from the same trade list using industry-standard methodology. Anyone with the raw trade list can reproduce these in Excel or Python.

Time-to-payout, Pay/y, Net $/y, Blow rate, and Viability in the sizing table come from a 1,500-path Monte Carlo v6 simulation over a 3-year horizon. Block bootstrap (5-day blocks) preserves serial autocorrelation of trade streaks.

Get Open + 5 more strategies.

Every Puravida Edge plan includes all 7 strategies and ongoing updates. Founders pricing: limited early-supporter Lifetime spots at 30% off.